Russia’s invasion of Ukraine upended global LNG markets last year—spurring Europe to buy record amounts of LNG, and pushing prices to their highest level ever

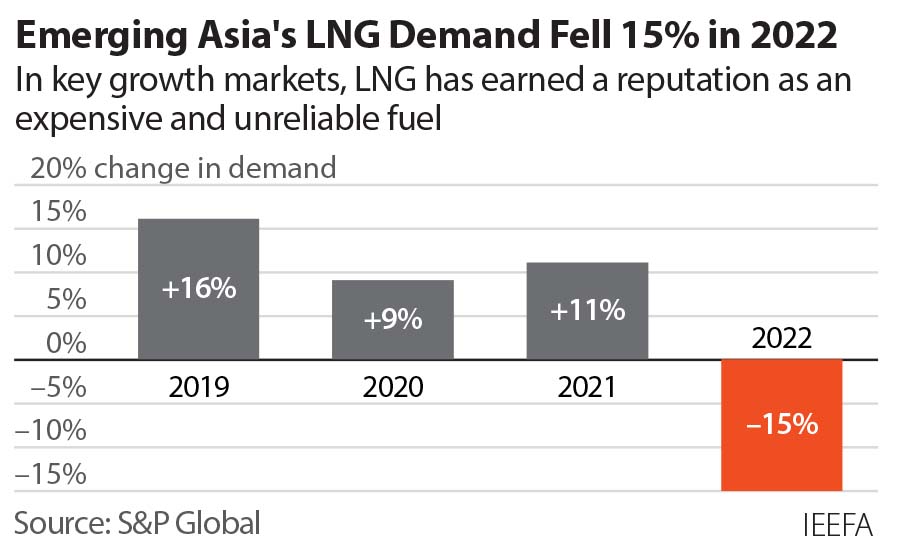

In Asia, LNG has earned a reputation as an expensive and unreliable fuel source, clouding future demand

The EU is taking aggressive steps to trim gas consumption, which could render new LNG import capacity unneeded

Although LNG markets may remain tight for several years, the global LNG market will see a wave of new projects coming online in 2025-27—potentially leading to a supply-demand mismatch and financial risks for LNG suppliers and traders

TTCT – Trong bối cảnh xung đột giữa các nước châu Âu và Nga, giá năng lượng ở Đức đã tăng vọt đến mức khiến đại đa số người Đức băn khoăn trước tình hình sinh hoạt trong mùa đông sắp tới.

Ảnh: Morning Consult

“Chúng ta lại vô địch thế giới”, một tay phóng viên giễu cợt trên truyền hình Đức, nhưng lần này không phải là chức vô địch World Cup hay số xe hơi bán ra. “Năng lượng của chúng ta có giá cao nhất thế giới”.

Tôi đã biết trước giá năng lượng ở Đức sẽ tăng cao, kể cả trước khi chiến tranh ở Ukraine nổ ra, nhưng “vô địch thế giới” thì quả là bất ngờ. Tượng trưng cho cuộc khủng hoảng hiện tại, mới đây tòa nhà Reichstag – trụ sở của chính quyền liên bang Đức – đã tắt đèn tối thui “làm gương” trong chuyện tiết kiệm năng lượng.

Suốt mấy thập niên qua, Đức hưởng lợi từ khí đốt giá rẻ của Nga thời Tổng thống Vladimir Putin. Còn năm nay, ngay cả trước khi hai đường ống cung cấp khí đốt chính là Dòng phương Bắc 1 và 2 gặp sự cố, Đức đã không nhận khí đốt từ Nga nữa, mà thay vào đó là từ các nước đồng minh như Hà Lan và Na Uy.

Trước cuộc chiến, Đức phụ thuộc nguồn cung từ Nga cho hơn 50% nhu cầu năng lượng (khí đốt và than đốt), nên cuộc khủng hoảng hiện giờ là dễ hiểu. Đây thậm chí được coi là mối đe dọa chưa từng thấy với cả nền kinh tế và sự giàu có của nước Đức kể từ Thế chiến II.

Giới lãnh đạo kinh tế và chính trị trong nước đột ngột nhận ra họ đã tham gia một cuộc chơi nguy hiểm và giờ đang phải trả giá đắt, theo đúng nghĩa đen.

A liquified natural gas (LNG) tanker leaves the dock after discharge at PetroChina’s receiving terminal in Dalian, Liaoning province, China July 16, 2018. REUTERS/Chen Aizhu//File Photo

SINGAPORE/NEW YORK, Oct 15 (Reuters) – Major Chinese energy companies are in advanced talks with U.S. exporters to secure long-term liquefied natural gas (LNG)supplies, as soaring gas prices and domestic power shortages heighten concerns about the country’s fuel security, several sources said.

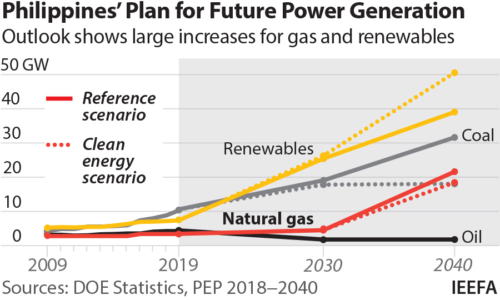

5 May 2021 (IEEFA Philippines): The race to develop liquified natural gas (LNG) facilities in the Philippines has gone from a marathon to a sprint but potential LNG investors must proceed at their own risk, according to a new report from the Institute for Energy Economics and Financial Analysis (IEEFA).

“Officials in the Philippines have endorsed a rapid buildout of LNG import infrastructure due to the anticipated depletion of the Malampaya deepwater development, the country’s only domestic source of natural gas, and high GDP growth expected over the next decade,” says the report’s author IEEFA Energy Finance Analyst, Sam Reynolds.

Exporting countries and industry players have pushed the narrative that natural gas, a fossil fuel alternative to coal, represents a viable transition fuel from coal to renewables. The United States, in particular, has encouraged legal and regulatory reforms to stimulate LNG demand creation.

LNG importers will bear climate-related risks of exporting countries, threatening energy security and electricity costs

The Texas energy crisis has become world news.

During last week’s extreme winter weather, surging electricity demand collided with falling generation, forcing the state’s grid operator to implement rolling blackouts. In many cases, blackouts lasted for over 24 hours, causing fuel and electricity supply shortages and disruptions throughout the gas supply chain. At least 4.5 million Texans were at one point without electricity and more than 30 deaths have been attributed to power losses, though the final toll could be much larger.

News of the Texas power crisis has spread throughout Asia, where energy growth markets such as Vietnam, the Philippines, and Bangladesh are considering U.S. liquified natural gas (LNG) imports as an alternative to coal-fired electricity generation. But the events in Texas have highlighted the risks inherent in LNG imports for both the energy transition and climate change adaptation.

Below are five lessons from the crisis for emerging markets in Asia.

Lesson 1. Gas/LNG volatility is here to stay.

It has been a tumultuous year in global LNG markets. The COVID-19 outbreak sent global LNG demand plummeting and Asian prices hit an all-time low of $1.85/MMBtu last May. U.S. LNG export facilities remained idle for much of the summer, oil and gas drilling fell by 40% internationally, and bankruptcies in the North American oil and gas sector soared to their highest level since 2016. Starting in the fall, a combination of production shut-ins, shipping delays, and cold weather caused Asian LNG prices to spike to a record high of $32.50/MMBtu.

The Texas energy crisis is another sign that volatility in global gas markets is likely to continue. High electricity demand combined with supply chain disruptions sent wholesale natural gas prices skyrocketing. At Texas’s Waha Hub, for example, prices jumped from $2.77 to $219, while spot prices in Oklahoma’s Oneok hub jumped to over $1,000/MMBtu. For gas producers able to keep wells operating, the Texas freeze was “like hitting the jackpot,” but for LNG exporters, power outages disrupted liquefaction trains and feedgas pipelines. Several LNG export terminals scaled back production, while Corpus Christi LNG and Cameron LNG went offline completely. Overall, 10 cargoes amounting to 1 billion cubic meters of gas were likely delayed from the already-volatile global LNG market.

Volatility in global gas markets is likely to continue

Lesson 2. Volatile prices can cause LNG-fired power plants in Asia and associated infrastructure to go under-utilised.

Volatile LNG prices create an increasingly challenging environment for price-sensitive emerging markets. High prices and difficulties sourcing gas can cause gas-fired power plants in importing countries to go underutilized. In turn, all the associated infrastructure – ports, regasification facilities, pipelines – are also at risk of being stranded. IEEFA recently estimated that volatile LNG prices put over $50 billion of natural gas projects at risk of cancellation in Vietnam, Bangladesh, and Pakistan.

Since the value of associated infrastructure is dominated by fixed costs, per unit natural gas prices depend largely on total gas demand. This means that to realize any economic benefits from imported gas, costs must be spread over a wider consumer base than currently exists in many south and southeast Asian countries. The decision to import LNG is therefore not an incremental one. Rather, it will lead to new sources of financial vulnerability resulting from long-term, large-scale fossil gas lock-in. Without major storage capacity, volatile LNG prices will be a constant threat to the affordability of gas and gas-powered electricity in import markets.

Lesson 3. LNG imports come at the cost of domestic energy security.

By importing greater volumes of LNG, Asian countries become more vulnerable to supply disruptions in global gas markets and geopolitical dynamics beyond their control. With increasingly severe and frequent weather events caused by climate change, Asian importers are not just assuming the risks of climate-related disruptions in their own country, they are also assuming risks of climate-related weather events in exporting countries. In Texas, generators were not required to invest in cold weather safeguards, leaving them vulnerable to unpredictable weather events.

LNG import infrastructure in Asia is highly vulnerable to extreme weather

LNG import infrastructure in Asia is also highly vulnerable to extreme weather. While numerous countries rely on floating storage and regasification units (FSRUs) as cheaper alternatives to land-based import terminals, FSRUs are difficult to operate in poor weather conditions. In 2018, Bangladesh announced it would cancel plans to build additional FSRUs because they were unreliable during the monsoon season. In Malta, the inoperability of FSRUs during storms has caused the complete shut-down of the country’s gas-fired power plants.

Lesson 4. Grid expansion and modernization must take centre stage.

Some commentators have suggested the solution to climate-related blackouts is to build more generation capacity, but all power sources are susceptible to outages when weather events occur. In Texas, 30,000MW of thermal capacity was forced offline – including 40% of natural gas capacity and a nuclear reactor – as well as 17,000MW of wind capacity. As a result, wholesale electricity prices skyrocketed to the state’s $9,000 per MWh cap, up from their average of $30.

Along with generation capacity, grid reliability depends largely on transmission infrastructure and interconnections to other areas. The Texas grid is highly isolated from surrounding power systems, limiting power imports from nearby markets. In small portions of the state connected to other grids, cities experienced brief blackouts compared to the rest of the state.

A greater emphasis on system-level planning in emerging Asian markets, rather than a myopic focus on generation, could improve the efficiency of existing generators, enable the installation of greater capacities of domestic renewable energy, and lower wholesale electricity prices during times of short supply.

Lesson 5. The energy transition is a humanitarian issue.

The COVID-19 pandemic and the Texas energy crisis have exacerbated the risks inherent in LNG imports and revealed the flaws of centralized generation capacity buildouts. In Texas, blackouts disproportionately affected low-income communities, while electricity bills for some households that maintained power spiked into the tens of thousands of dollars. The total cost of electricity sold in Texas from February 15-19 was $50.6 billion, up from $4.2 billion in the prior week. For Asian countries already grappling with high electricity prices, the risks of LNG imports and associated infrastructure lock-in are simply too high. Instead, reliability and resilience are key to keeping costs down and the lights on.

The winter storms that swept across the U.S., particularly Texas, upending the energy market and knocking out power for millions of people, have delivered a windfall for Macquarie Group, with the Australian bank lifting its profit outlook for 2021 by as much as 10 percent, just two weeks after warning that earnings would be “slightly down”.

“Extreme winter weather conditions in North America have significantly increased short-term client demand for Macquarie’s capabilities in maintaining critical physical supply across the commodity complex,” according to the company, which is the second-largest supplier of gas in North America after oil major BP, as quoted by Reuters.

TheLEADERCác dự án nhiệt điện khí LNG sẽ gặp nhiều khó khăn khi triển khai hơn so với các dự án nhiệt điện than – vốn đã phải đối mặt với tình trạng chậm tiến độ triền miên, theo Viện Kinh tế Năng lượng và phân tích tài chính (IEEFA).

Toàn cảnh một nhà máy Nhiệt điện sử dụng khí LNG.

Trong thời gian vừa qua, Việt Nam đã nhanh chóng nổi lên là một trong những thị trường nhập khẩu khí thiên nhiên hóa lỏng (LNG) cho phát điện tiềm năng nhất ở châu Á.

Các dự án LNG đều yêu cầu được bao tiêu dài hạn. Trong ảnh: Mặt bằng một dự án điện khí LNG hoàn chỉnh

Khó đàm phán

Trao đổi với phóng viên Báo Đầu tư mới đây, một quan chức của Cục Điện lực và Năng lượng tái tạo (Bộ Công thương) cho hay, Dự án Điện khí LNG Bạc Liêu đã không thể ký được PPA trong năm 2020. Như vậy, kỳ vọng về việc “đàm phán PPA ngay trong tháng 8/2020 và ký kết PPA vào cuối năm 2020” đã không thành hiện thực.

By Dat Nguyen November 23, 2020 | 10:50 am GMT+7 vnexpressAn LNG tanker passes by the Strait of Singapore. Photo by Shutterstock/Igor Grochev.Several foreign and domestic companies have expressed interest in building multibillion-dollar liquefied natural gas power and storage plants in the central province of Khanh Hoa.

Four foreign firms, Millennium Group of the U.S., Sumitomo Corporation and J-Power of Japan and a venture between Vietnam’s Embark United and the U.S.’s Quantum, want to build plants in the Van Phong Economic Zone, province authorities said in a recent statement.

Millennium wants to build a 9,600-MW power plant and storage complex at a cost of $15 billion.

J-Power, which has been in the energy sector for 60 years, is eyeing a 3,000-MW, $3.2-billion plant that will be commissioned by 2025.

Embark-Quantum seek to build a 6,000-MW plant and storage complex on 300 hectares.

Several Vietnamese companies have also expressed interest in building LNG power and storage projects in the economic zone.

National utility Vietnam Electricity (EVN) has proposed a 6,000-MW plant, while the Vietnam National Petroleum Group (Petrolimex) has proposed an LNG storage complex with a capacity of three million tons a year.

A joint venture between four Vietnamese companies has sought to build a 1,500-MW plant.

Khanh Hoa authorities said they have earmarked 1,000 ha of land in the economic for LNG projects, and plan to ask the Ministry of Industry and Trade to add it to the national power plan for 2021-2030.

Vietnam’s government is drafting a new national power development plan for the next decade that will include 22 LNG power plants with a combined capacity of up to 108.5 GW, the first of which will be commissioned in 2023.Related News:

Wednesday, October 28, 2020, 16:44 GMT+7 Tuoitrenews

The logo of the multinational electric power company AES is seen at an office in Santiago, Chile June 4, 2019. Photo: Reuters

HANOI — AES Corp. will sign a deal with PetroVietnam Gas GAS.HM to develop a $2.8 billion liquefied natural gas (LNG) import terminal and a power plant in Vietnam, U.S. Secretary of State Mike Pompeo said on Wednesday.

By Dat Nguyen October 3, 2020 | 02:30 pm GMT+7 vnexpressAn LNG carrier seen at the port of Nakhodka, Russia. Photo by Shutterstock/VladSV.

The northern port city of Hai Phong has given approval to Exxon Mobil to build a liquefied natural gas-fired power plant.

The city People’s Committee said in a recent statement that the $5.09 billion plant will be built in two phases, each with a capacity of 2.25 gigawatts, the first going on stream in 2026-27 and the second three years later.

– Trong bối cảnh nguồn cung khí trong nước suy giảm nhanh, các mỏ mới có chi phí phát triển cao, quá trình đàm phán giá khí thường kéo dài, trong khi đó nhu cầu sử dụng khí ngày càng tăng đòi hỏi phải có các giải pháp đồng bộ để bảo đảm duy trì nguồn cung cấp khí ổn định, lâu dài cho nền kinh tế và góp phần vào bảo đảm an ninh năng lượng quốc gia. Do đó, giải pháp hữu hiệu nhất là ưu tiên đầu tư hạ tầng kỹ thuật phục vụ nhập khẩu và tiêu thụ khí tự nhiên hoá lỏng (LNG) như đã nêu trong Nghi quyết 55/NQ -TW của Bộ Chính trị.

Khí tự nhiên được coi là nhiên liệu hóa thạch thân thiện hơn với môi trường vì phát thải CO2 thấp nhất tính trên cùng một đơn vị năng lượng và thích hợp để sử dụng cho các nhà máy nhiệt điện công nghệ tua bin khí hỗn hợp (TBKHH). Tính theo nhiệt lượng tương đương, thì đốt khí tự nhiên sẽ sinh ra một lượng CO2 ít hơn khoảng 30% so với đốt dầu và 50% so với đốt than, còn với NOx thì có thể giảm tới 90% và bụi 100%.

Trong những năm gần đây, đặc biệt từ sau COP 21 nhu cầu LNG trên thế giới tăng đáng kể. Năm 2016, khối lượng LNG buôn bán trên toàn thế giới khoảng 258 triệu tấn LNG, tăng 13 triệu tấn so với năm 2015 (5,3%) và giai đoạn 15 năm từ 2000 đến 2015 nhu cầu LNG trên thế giới tăng với nhịp độ bình quân 6,3%/năm. Theo dự báo, công suất LNG trên thế giới sẽ tăng từ 340 triệu tấn/năm (năm 2017) lên 453 triệu tấn/năm vào năm 2022.

2019 was another dynamic year for the global LNG market. The market saw some demand growth, although not as much as expected, particularly in Asia, driven largely by China. There has also been sustained pressure on prices, with spot prices dipping to new lows in Asia in the latter half of the year, which has continued into 2020. Portfolio players have gone from strength to strength, cementing their place as key drivers of current market trends, and we have seen a number of traders taking steps to broaden their activities and firm up their place as a portfolio player.Tiếp tục đọc “ENERGYSOURCE | ISSUE 22 06 FEB 2020LNG contracting: Recent trends and the outlook for 2020”→

An LNG tanker passes by the Strait of Singapore. Photo by Shutterstock/Igor Grochev.Several foreign and domestic companies have expressed interest in building multibillion-dollar liquefied natural gas power and storage plants in the central province of Khanh Hoa.

An LNG tanker passes by the Strait of Singapore. Photo by Shutterstock/Igor Grochev.Several foreign and domestic companies have expressed interest in building multibillion-dollar liquefied natural gas power and storage plants in the central province of Khanh Hoa.

An LNG carrier seen at the port of Nakhodka, Russia. Photo by Shutterstock/VladSV.

An LNG carrier seen at the port of Nakhodka, Russia. Photo by Shutterstock/VladSV.